The Unseen Crisis Behind the Headlines

One month into the war in Iran, the world faces a shortage that extends far beyond crude oil. The conflict has disrupted flows through the Strait of Hormuz, reducing global supply by roughly one-fifth. While headlines focus on rising gasoline prices, a more insidious shortage threatens daily life across continents. The restriction of oil and natural gas flows has triggered a cascading failure in petrochemical supply chains, squeezing the materials needed to manufacture shoes, clothing, medical devices, and food packaging.

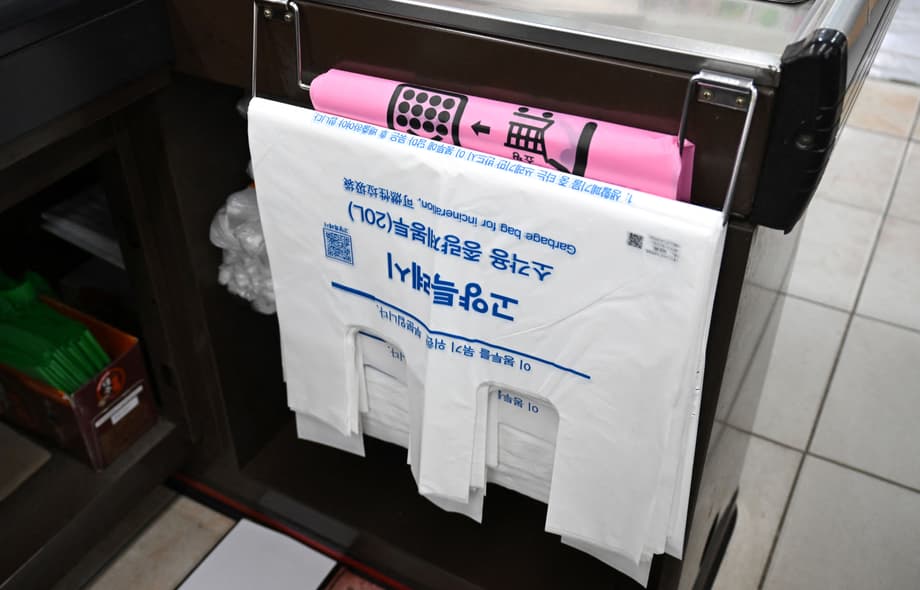

Asia feels the impact most acutely. The region accounts for more than half of global manufacturing and relies heavily on imported commodities. In South Korea, citizens have resorted to panic-buying trash bags. Taiwan has established emergency hotlines for manufacturers out of plastic materials. Japanese hospitals fear running short of dialysis tubes. The crisis demonstrates how quickly energy disruptions translate into consumer goods shortages when supply chains stretch across oceans.

The interconnected nature of modern manufacturing means that petroleum derivatives serve as the hidden substrate of production. Adhesives for footwear, industrial lubricants, solvents for paints, and plastic resins all derive from the same naphtha feedstocks now stranded in the Persian Gulf. When these inputs vanish, assembly lines slow regardless of whether the final products seem related to energy.

Dan Martin, co head of business intelligence at Dezan Shira & Associates, an advisory firm specializing in Asian markets, describes the rapid transmission of economic shocks from energy to finished goods.

This spills into everything very, very quickly: beer, noodles, chips, toys, cosmetics.

The International Monetary Fund recently warned that such complex spillovers confront economies with limited shock absorption capacity. In a blog post, the organization stated that all scenarios lead toward higher prices and slower growth. Countries have begun releasing historic amounts of oil from emergency stockpiles, but these reserves cannot address the specific shortage of naphtha, the petroleum byproduct that serves as the building block for synthetic materials.

Why Naphtha Matters More Than Crude

The shortage of naphtha distinguishes this crisis from typical oil shocks. Naphtha, a petroleum byproduct, serves as the critical feedstock for synthetic materials. Unlike crude oil, which nations can release from strategic reserves, naphtha lacks ready substitutes. Producers maintain minimal inventories of this specialized feedstock. When the Strait of Hormuz closed, Asian petrochemical plants lost their primary supply line almost immediately.

Jim Fitterling, chair and CEO of Dow, addressed the severity of the situation at the CERAWeek by S&P Global conference in Houston. He explained that roughly twenty percent of global petrochemical capacity faces blockage from the effective closure of the Strait of Hormuz.

The die is being cast for the rest of the year for what is going to happen in the markets. It is like the unwind we saw on supply chains during COVID. You could be in the 250- to 275-day range. This is not going to be an instantaneous rewind.

The geographic distribution of feedstock sources creates a divided global economy. Commodity petrochemical plants in the Western Hemisphere, particularly the United States, rely on natural-gas-derived ethane. This supply remains unaffected by the Middle East conflict. Asia and much of Europe depend on crude-oil-based naphtha. Nearly half of Asian naphtha supplies normally flow through the Strait of Hormuz.

Consequently, Asian facilities have begun declaring force majeure, a legal term indicating that unforeseeable circumstances prevent contract fulfillment. Several plants have cut output drastically or suspended operations entirely. South Korea has imposed export bans on naphtha to preserve domestic supply. The country has also purchased its first load of naphtha from Moscow since the Ukraine war began, taking advantage of suspended sanctions on certain Russian petroleum products.

Medical Supplies and Food Security Under Threat

The petrochemical shortage threatens critical medical infrastructure. In Japan, hospitals worry that patients with chronic kidney failure may face treatment disruptions due to shortages of plastic medical tubes used in hemodialysis. Malaysian glove manufacturers report that a lack of petroleum byproducts needed to make rubber latex endangers global supplies of medical gloves. These are not luxury items but essential components of modern healthcare.

The crisis extends into food production through fertilizer shortages. The Middle East supplies forty-five percent of global sulphur, used in fertilizer manufacturing, and twenty-two percent of urea and ammonia, essential crop nutrients. Morgan Stanley data indicates that roughly one-third of global fertilizer trade passes through the Strait of Hormuz. US farmers already pay one-third more for imported urea since the war began.

In Asia, rice farmers face impossible choices. Harvest-ready fields lie idle across Southeast Asia because farmers cannot afford the diesel to run tractors or the fertilizer to nourish crops. Some Thai farmers leave rice in the ground rather than pay exorbitant harvesting costs. The United States Department of Agriculture notes that American farmers plan to plant less corn and more soybeans this year, switching to less nutrient-intensive crops.

India provides a case study in cascading failures. The government mandated gas supply curbs on March 9, prioritizing domestic cooking fuel over industrial users. Reliance Industries cut aromatics production, potentially losing seventy-five thousand tonnes of paraxylene. Bharat Petroleum halted acrylic acid production. The Gas Authority of India Limited shut down polyethylene units. These shutdowns affect packaging for food, medicine, and consumer goods.

Infrastructure Projects Grind to a Halt

The shortage of bitumen and liquid diesel oil has stalled road construction across India. In Rajasthan, contractors working on National Highway 27 and NH 148D report severe asphalt shortages. One contractor noted that projects valued at nearly six hundred crore rupees face serious delays. Asphalt prices have risen from roughly forty thousand rupees per tonne to above fifty thousand, with supplies remaining irregular even at elevated prices.

Shortages of immersion oil and liquid diesel oil, used to run heavy construction equipment, compound the problem. Against estimated requirements of twenty-seven lakh litres across multiple projects, only about ten lakh litres have arrived. Prices climbed from forty-five thousand to sixty thousand rupees per tonne. The National Highways Authority of India acknowledges that work has slowed sharply, with contractors advised to continue other activities wherever possible to prevent total project halts.

In Indonesia, the Prabowo administration faces a moment of truth. The energy crisis threatens to turn into a severe cost of living emergency. The government has refused to scale back its twenty billion dollar free nutritious meal program despite the fiscal strain. Finance Minister Purbaya Yudhi Sadewa has raised the possibility of increasing the budget deficit limit beyond three percent of GDP. Economists warn that without spending cuts, the deficit may reach three point six percent.

Global Disparities in Resilience

The crisis has created a two-speed global economy. While Asian manufacturers struggle with feedstock scarcity, Western Hemisphere producers enjoy competitive advantages. North American petrochemical plants run on domestic natural gas, giving them cost advantages even under normal circumstances. With Asian prices soaring, the arbitrage between US and Asian markets has exploded from less than five hundred dollars per metric ton to above one thousand two hundred dollars.

John Moseley, chief commercial officer of Port Houston, reported a twelve percent increase in exports in just two weeks, particularly polyethylene shipped in containers. Analysts expect huge increases in exports to Asia as the year progresses. However, even maximum capacity operation in the Americas cannot fill the gap left by missing Middle Eastern and Asian production.

China presents a complex case. The country entered the crisis with substantial oil reserves, enough for one hundred thirty days of consumption. Beijing has prohibited most petroleum product exports, preserving domestic supply while potentially starving trade partners of diesel and jet fuel. This creates diplomatic tensions with Southeast Asian nations that depend on Chinese fuel exports. Australia, a major supplier of lithium and iron ore to China, faces growing diesel shortages that could disrupt mining operations.

Europe faces different pressures. While the continent does not rely heavily on direct Gulf flows, it remains exposed to global price shocks. Anup Kothari, a BASF executive board member, noted that the region experiences less pressure from imports, which had been problematic in recent years. So far, the situation appears as a net positive for European producers, though everyone expects the full effects to materialize soon.

The Long Road Back to Normalcy

Even if hostilities cease tomorrow, recovery will take months or possibly the remainder of the year. Roughly four hundred thirty vessels remain stranded in the Persian Gulf, with over three hundred being oil tankers. When the strait reopens, authorities will prioritize oil and gas shipments, followed by fertilizers for agriculture. Petrochemical tankers rank lower in the pecking order and require four-week voyages to Asia.

Andrew Neale, global head of chemicals for S&P Global Energy, warned that the chemical industry will face severe supply chain dislocation. Containers will accumulate in the wrong locations, requiring quarters rather than months to unwind. The industry may see demand swings similar to those following the COVID pandemic.

J.P. Morgan analysts described the shock as unfolding sequentially rather than simultaneously, a rolling supply disruption moving westward. Asia has moved beyond the preventive phase into active scarcity management. The last crude deliveries sent before the war arrived in early April. From that point forward, the physical absence of materials will force harder choices than price management.

Some manufacturers hope to outlast the crisis by delaying purchases, betting that prices will fall if the conflict resolves. Qiu Jun, a polyester maker in Haining, China, has seen polyester chip prices jump fifty percent. His factory runs only to fulfill existing orders while he avoids overpaying for unwanted stock. The cautious approach carries risks. As Shariene Goh, senior petrochemical analyst at ICIS, noted, end-products segments might rely on their inventory levels, but these will deplete over time. Consumer goods depending heavily on plastic packaging may start running out soon.

What to Know

- The Iran war has effectively closed the Strait of Hormuz, disrupting twenty percent of global oil supply and blocking nearly half of Asian naphtha imports.

- Naphtha shortages have forced Asian petrochemical plants to declare force majeure and cut production, affecting plastics, medical supplies, and food packaging.

- Global medical supply chains face shortages of dialysis tubes, latex gloves, and IV bags due to petroleum byproduct scarcity.

- Fertilizer shortages threaten rice harvests across Southeast Asia and raise food security concerns worldwide.

- Western Hemisphere producers using natural gas feedstocks enjoy cost advantages while Asian manufacturers struggle with supply constraints.

- Recovery timelines extend 250 to 275 days even if the conflict ends immediately, due to shipping backlogs and supply chain dislocation.