How AI turned electricity into the new bottleneck

Artificial intelligence is moving out of the lab and into massive clusters of computers known as data centers. Model training and the delivery of AI queries concentrate thousands of high performance chips in one place. That equipment draws heavy electricity and throws off heat, which then requires industrial cooling. Electricity, not algorithms, has become the binding constraint in many locations.

- How AI turned electricity into the new bottleneck

- Why Chinese equipment makers are in demand

- The numbers behind the surge

- From transformers to switchgear, what buyers need now

- Where orders are coming from

- What this means for investors and markets

- Risks, policy shifts, and quality checks

- Can supply keep up with the AI buildout

- What to Know

Energy agencies estimate that data centers already consume about 415 terawatt hours of electricity in 2024, roughly 1.5 percent of the world total. In its base case, the International Energy Agency projects that figure could roughly double to around 945 terawatt hours by 2030. The United States, China, and Europe are the largest users today. The United States and China alone are set to account for nearly 80 percent of the growth through 2030. Concentrated loads challenge local grids and require costly upgrades.

AI servers rely on powerful graphics processors that pull more power per rack than conventional computing. Higher power density pushes up the need for transformers, switchgear, cables, fault protection, and cooling. Many utilities also ask for on site backup and energy storage to ensure reliability when data centers ramp quickly. The result is a fast growing order book for companies that build the equipment which moves electricity from power plants to server rooms.

Why Chinese equipment makers are in demand

A wave of AI related construction is colliding with geopolitical limits and long lead times. Large tech firms in the United States continue to buy from allies in Japan and South Korea rather than mainland suppliers. Order books at those companies have stretched to years, which pushes buyers in other markets to look to China for faster delivery and lower cost.

Pierre Lau, China equity strategist and head of Asian utilities and clean energy research at Citigroup Global Markets, has tracked how this shift filters through equipment supply.

“The US buys products from Japan and South Korea instead of China amid geopolitical tensions. Now the pipeline for Japanese and Korean firms is as long as three years, so companies from emerging markets turn to mainland suppliers.”

He also argued that the present cycle for mainland suppliers could persist while the White House continues to back aggressive AI buildouts by large cloud and telecom investors.

“[The upcycle will be sustained] as long as Trump remains the person in charge.”

Export data reflect the surge. In the first ten months of the year, China shipped about 7.3 billion United States dollars of transformers and around 4.3 billion United States dollars of high voltage gas insulated switchgear, gains of 37.8 percent and 28.5 percent over the same period a year earlier. By comparison, total exports grew 5.3 percent.

The numbers behind the surge

The pressure is most acute in North America. Industry estimates suggest data center projects could cause a power shortfall of up to 20 percent through 2028 if generation, transmission, and distribution do not expand in time. Capital spending plans by large cloud providers have ramped sharply, and analysts expect grid investment to rise around 5 percent a year this decade. Some researchers forecast that AI related power demand could expand by an order of magnitude by 2026, which would drive another leg of demand for transformers and switchgear.

Forecasters are also raising expectations inside China. UBS now projects the country’s electricity demand to grow about 8 percent a year from 2028 to 2030. Its research attributes roughly 2.3 percentage points to AI data centers, 1.4 points to export oriented manufacturing, and 1.2 points to electrification of transport and industry. China plans about 5 to 6 gigawatts of new AI data center capacity in the next three years, far below the 40 to 45 gigawatts now in the pipeline in the United States, which suggests room for further growth. UBS expects a new capital spending cycle in the 15th Five Year Plan with power investment growing near 12 percent a year, from nuclear approvals and wind additions to grid expansion and storage.

The excitement has spilled into equities. Shares of electrical component producer TBEA jumped nearly 30 percent across a standout week in November, while solar equipment maker CSI Solar surged more than 40 percent in the same period. Investors are rotating from chip design and pure AI software toward the infrastructure that makes compute possible, including power, metals, cooling, and storage.

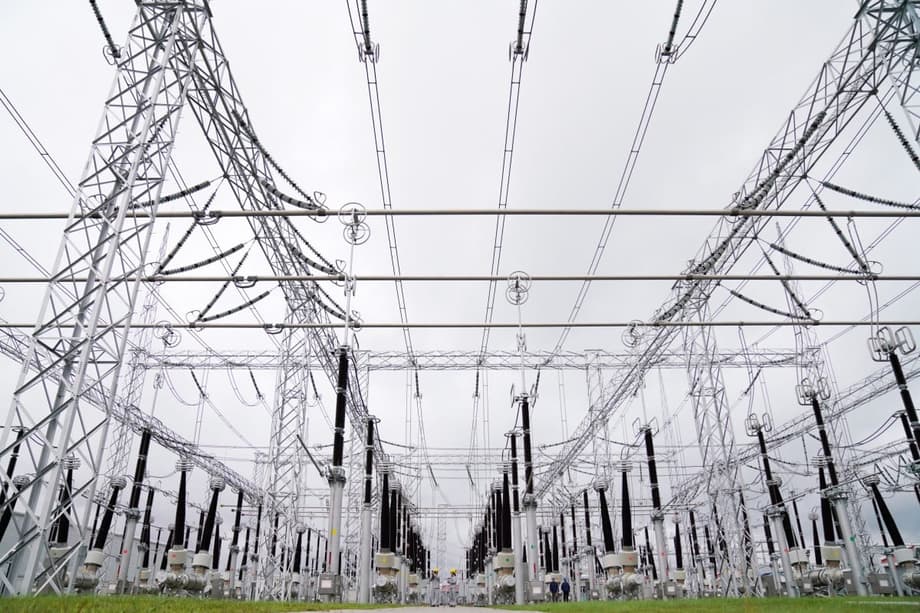

From transformers to switchgear, what buyers need now

Behind the headlines, the shopping list for a large AI facility spans an entire substation and then some. Many sites require their own high voltage connection and on site equipment that looks like a miniature grid.

- Power transformers: These step up voltage for transmission and step down voltage for servers. Lead times can run many months because cores use grain oriented electrical steel and the units must pass exacting tests.

- Gas insulated switchgear (GIS): Sealed enclosures save space and improve reliability in dense urban sites or harsh climates. They manage high fault currents and allow safe switching of heavy loads.

- High voltage direct current (HVDC): As data center hubs grow, some grids use HVDC to bring large blocks of power from distant generation. That calls for converters, control systems, and specialized transformers.

- Medium voltage gear and power distribution units: These distribute power safely across buildings and between racks, with coordinated protection to prevent outages.

- Cooling and thermal management: Chillers, evaporative systems, and liquid cooling keep chips within safe temperatures as power density rises.

- Energy storage systems: Battery banks absorb short spikes in demand, provide fast response, and help maintain uptime during grid fluctuations.

- Cables and conductors: Large cross section copper and aluminum cables connect equipment within facilities and to the grid. Rising grid construction has lifted demand for cable aluminum.

Chinese manufacturers compete in many of these products. Their cost base, scale, and experience with large domestic grid projects allow them to quote aggressively, especially where buyers face long queues elsewhere.

Where orders are coming from

North America is the most visible demand center. Analysts expect utilities to rely on gas turbines for quick capacity in the short term, while longer term additions will include gas fired and nuclear plants and extensive grid upgrades. Transformer supply gaps are widening as older coal and gas plants retire and as connection queues grow.

Emerging markets are adding another layer. Countries in Latin America, the Middle East, and Southeast Asia are building generation and upgrading transmission to support industrial growth and new data centers. Many of these markets are price sensitive and time constrained, which creates an opening for mainland exporters.

Data center developers tend to cluster around access to cheap electricity, reliable connections, and friendly permitting. That has drawn projects to places with hydro, nuclear, or large renewable fleets. Chinese companies often act as component suppliers to international contractors or as direct exporters, filling gaps in transformers, GIS, and high current cables.

What this means for investors and markets

The shift has an investment angle. As enthusiasm for pure AI names cools after strong rallies, a growing set of investors is hunting for companies tied to electricity supply chains. This includes grid equipment makers, energy storage providers, and metals producers that supply copper and aluminum.

China offers multiple listed plays. The week when TBEA and CSI Solar rallied highlighted that theme. If grid spending follows through, order visibility for transformer and switchgear makers could extend for years. Pricing power may improve in niches where lead times are long and quality requirements are stringent.

There are still constraints. Utilities and cloud operators operate on different timelines. Large plants and transmission lines take years to permit and build, while data center teams move in months. Share prices will also track commodity swings and any changes in export policy in large consuming regions.

Risks, policy shifts, and quality checks

Trade barriers can change the calculus. Higher tariffs, buy local rules, or new security reviews could limit shipments to some markets. Governments are sensitive about the origin of equipment that sits inside critical infrastructure.

Quality and standards matter as much as price. Buyers specify adherence to IEC or IEEE standards and often insist on factory inspections, type tests, and on site commissioning support. Strong warranties and service networks are essential for high voltage gear that must run for decades.

Input costs are another variable. Copper, aluminum, and grain oriented electrical steel are core to transformers and cables. If these rise sharply, margins can compress even with a strong order book. Renewable projects and electric vehicle growth also draw on the same materials, which can tighten supply.

Can supply keep up with the AI buildout

The mismatch between fast AI adoption and slow energy infrastructure is real. A large transformer can take 12 to 24 months to build after order, then transport and installation add more time. Factory expansions require new equipment, trained welders, and consistent steel supply.

Efficiency improvements can help. Better power usage effectiveness in data centers and more efficient accelerators can reduce the energy per unit of compute. The International Energy Agency still expects data center consumption to grow faster than other sectors through 2030 in its base case, with the United States and China driving most of the increase. That forecast highlights the need for steady grid investment and procurement planning.

Stopgap solutions are already in use. Developers are pairing data centers with battery storage to smooth load swings and secure backup, adding on site generation such as gas turbines or solid oxide fuel cells where allowed, and contracting for power from new wind and solar farms. Transmission planners are expanding the use of high voltage direct current to move large blocks of power to new computing hubs. Additional nuclear capacity in the United States is unlikely to arrive before 2028 to 2030, which means the pressure on transformers and switchgear will remain elevated for several years.

What to Know

- AI data centers are reshaping electricity needs, lifting demand for transformers and switchgear worldwide.

- Chinese exports of transformers and gas insulated switchgear rose 37.8 percent and 28.5 percent in the first ten months, beating a 5.3 percent gain in total exports.

- Analysts say US buyers favor Japanese and Korean suppliers, whose backlogs stretch to years, prompting emerging markets to turn to mainland vendors.

- The International Energy Agency projects data center electricity use could roughly double by 2030, with the United States and China driving most of the increase.

- Industry estimates point to a potential power shortfall in the United States of up to 20 percent from data centers through 2028 if supply lags.

- UBS now sees China’s electricity demand rising about 8 percent a year in 2028 to 2030, with 2.3 points coming from AI data centers.

- Investors are rotating toward power equipment, storage, and metals, with Chinese names among the beneficiaries.

- Risks include tariffs and security reviews, long manufacturing lead times, and swings in copper, aluminum, and electrical steel costs.